ArcelorMittal : A de-carbonization story

“Heads I win; Tails I don’t lose much.” - Mohnish Pabrai

Investment Summary: ArcelorMittal (AM) is trading at less than 5 times of operating earnings in a depressed steel demand environment at ~18B USD. In the normalized environment the earnings are expected to be 20-25% higher. In the next 7 years, the decarbonization capex will generate higher EBITDA of 1.8B$ by 2026, and subsequently the company can generate 10B$ of EBITDA (6.5B in 2023 + 1.8B additional earning by 2026 + 1.7B$ additional EBITA from the capex from 2027 to 2030 and inflation) in a bad environment in 2030. With 5x EBITDA multiple would result in 50B$ market cap; ~3x from the current market price and share count reduction by 50% through share buybacks would result in 6x return by 2030.

Business & History

ArcelorMittal (NYSE:MT) was created by the takeover of Western European steel maker Arcelor (Spain, France, and Luxembourg) by Indian-owned multinational steel maker Mittal Steel in 2006. ArcelorMittal is the second largest steel producer in the world, with an annual crude steel production of 78 million metric tones as of 2022.

ArcelorMittal Geographical Presence:

Americas : 39%

Western Europe: 50%

Rest of the world South Africa and Ukraine: 11%

2. Steel Making basics

Blast Furnace-Basic Oxygen Furnace (BF-BOF) route: This is the traditional method for steelmaking, responsible for about 70% of global steel production. It involves two main steps:

Blast Furnace: Iron ore, coke (purified coal), and limestone are heated to extremely high temperatures in a blast furnace. The intense heat causes a chemical reaction that separates the iron from the oxygen in the iron ore, producing molten iron (pig iron) along with slag (impurities).

Basic Oxygen Furnace (BOF): The molten iron from the blast furnace is then transferred to a Basic Oxygen Furnace (BOF). Here, pure oxygen is blown into the molten iron, which burns off impurities like carbon, silicon, and manganese. Alloying elements are then added to the steel to achieve specific properties.

Electric Arc Furnace (EAF) route: The EAF process is a more recent method that uses electricity to melt scrap steel or a combination of scrap and direct reduced iron (DRI). EAF steelmaking is considered more environmentally friendly because it uses a lower percentage of virgin raw materials and less energy compared to the BF-BOF route.

Key differenences of steel making process (Source: Google Gemini)

| Feature | BF-BOF | EAF |

|---|---|---|

| Raw Material | Iron ore, coke, limestone | Scrap steel, DRI |

| Heat Source | Combustion of coke | Electricity |

| Environmental Impact | Higher CO2 emissions | Lower CO2 emissions |

| Dominant use | Mass production of steel | Specialty steels and construction steel |

Role of DRI and HBI

DRI and HBI in steelmaking go hand-in-hand. They represent different stages in the same process:

Direct Reduced Iron (DRI): This is the initial product. Iron ore is exposed to a reducing gas (often natural gas) in a controlled environment. This process removes oxygen from the iron ore, transforming it into a porous, sponge-like material with a high iron content (around 90%).

Hot Briquetted Iron (HBI): DRI is a valuable product, but it's difficult to transport due to its high porosity and reactivity. To address this, DRI is often compressed into dense briquettes at high temperatures (above 650°C). This process creates HBI, which is much easier to handle and store.

How are DRI/HBI used in steelmaking?

Both DRI and HBI can be used as a feedstock in different steel making furnaces:

Blast Furnace (BF): In the traditional BF-BOF route, DRI/HBI can partially replace iron ore, reducing the amount of energy needed for the initial reduction process.

Electric Arc Furnace (EAF): EAFs primarily rely on scrap steel for melting. However, DRI/HBI can be a good substitute, especially when high-quality scrap is limited. Additionally, DRI/HBI can help EAFs achieve specific steel properties.

Benefits of DRI/HBI:

Lower emissions: Compared to traditional methods using blast furnaces, DRI/HBI production can have a lower carbon footprint.

Flexibility: DRI/HBI can be used in both BF and EAF steelmaking, offering greater flexibility to producers.

High-quality steel: DRI/HBI can be a source of high-purity iron for steel production.

Overall, DRI/HBI plants are becoming increasingly important in the steel industry as a way to produce steel more efficiently and with a lower environmental impact.

3. Macro outlook

The United Nations forecasts a global population of almost 10 billion in 2050. At today’s apparent steel use per capita, that will require an annual steel production of around 2.2 billion tons. However, many forecasts also anticipate a surge in steel demand per capita in populous regions such as India or Africa. This could drive steel production up to around 2.75 billion tons per year, expected to grow at 3-4% CAGR.

CO2 Emissions per ton of steel production based on the manufacturing process:

BF-BOF: 1,900Kg

DRI:650Kg

EAF: 140Kg

Source: https://www.sms-group.com/insights/all-insights/the-steel-industry-in-2050

Considerable investments are required for de-carbonization to move to DRI and EAF based steel production

4. Business Parameters

| Business Parameter | Value | Comments |

|---|---|---|

| Market Cap | $ 19B | |

| Enterprise Value | $ 18.5B | |

| Debt Cash Net Debt |

$ 10.2 B $ 5.8B ($ 11.4B liquidity) $5.2B |

|

| Revenue Growth (1, 3, 5 Years) | -14%, 6.5% , -2.7 % | After Covid-19 demand surge, there is continuous destocking in the industry coupled with China dumping. |

| Operating Income (EBIT) (1, 3, 5 Years) | -64% , -15% , -14 % | |

| Cash from operations in 2023 | $ 6.5B | |

| Gross Margin - EBITDA/Ton | EBITDA/t increased by +$35/t to $145/t in 1Q’24 vs 4Q’23 | |

| Capex Guidance | ~4.5B (traditional + decarbonization) | Decarbonization capex expected to be 10B$ in the next 5-6 years. |

5. Management

The company is run by Lakshmi N Mittal and his son Adithya Mittal. The management and family members own 42% of the company stake. The company grew by M&As.

Positives:

Got skin in the game (42% company ownership)

Keeping lean balance sheet, net debt of 4.5-5B$ < 1x EBITDA

Share buy backs aligned with minority share purchases

Decarbonization: Management realized that to stay in business they have to decarbonize the steel making process.

Negatives:

Venture into countries like Kazakhstan lead to impairments and asset take over by the government at low price.

Don’t like too many JVs. As of today the JVs generate 4.5B$ worth of EBITDA.

6. Company Focus

Company focuses on Steel manufacturing and owns iron mines in Canada and Liberia. The company clearly stated that they are not interested in metallurgical coal mines.

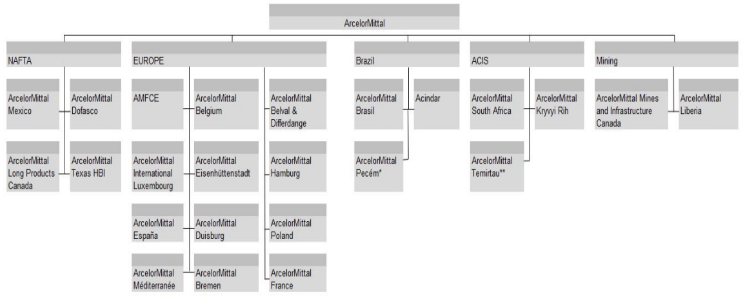

Org-Structure:

Source: Annual Report - 2023

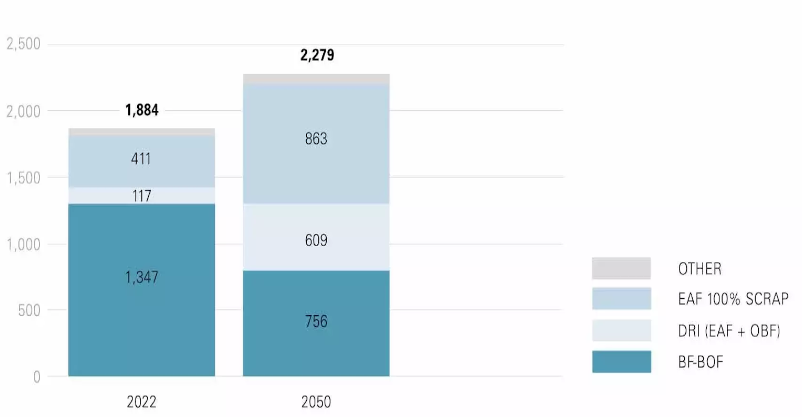

De-Carbonization:

The steel industry is gradually moving towards de-carbonization, requiring huge capex in the upcoming years. Here is the AM de-carbonization plan until 2050. The near term CAPEX spend will be on DRI and EAF transition.

Source: Annual Report - 2022

High Fixed cost business - Operating deleverage if capacity utilization comes down. The following table highlights that capacity utilization in 2023 is very low; 25% to 63% based on the product segment. If we look at 2021 utilization, it ranges from 24% to 84% which is considerably high.

2021 Cash from Operations: 9.9B$

2023 Cash from Operations: 7.6B$ (down 24% from 2021)

Source: Annual Report - 2023

On-going Capex:

The projects focus on de-carbonization, renewal energy, and high-value products. Most of the capex projects are scheduled to complete in 2024. The company expects to generate 1.8B$ of additional EBITDA from these projects.

Source: Annual Report - 2023

Sustainable Solutions Group(SSG):

AM started Sustainable Solutions Group to develop a portfolio of final products utilizing more sustainable steel, and capturing green premium.

For example steel costs <10% of the cost of a car, and consumers are willing to pay 200 Euros more for green steel.

In 2023, SSG generated an EBITDA of 368m$ and AM expects SSG’s EBIDTA to double by year 2028 as there is a strong demand for Green Steel.

7. Positive Triggers to company’s earnings

Increasing steel production capacity in India to 15MT from 9MT by 2026 to address the growing needs of India infrastructure (to be executed by JV AM/NS).

The Ukraine plant is still not making money, once the war stops there could be potential addition to the bottomline.

More under-construction projects to come online during 2024.

66$/share book value whereas the company currently trades at 23$. The share buyback to impact positively to the existing shareholders.

The company is doing share buy back at aggressive pace, repurchased 36% of the shares outstanding from Sept 2020 until Q2 2024.

AM is investing in renewable energy through JVs for captive consumption which in-turn would improve the operating margins of steel making. These power investments are recurring in nature with high operating margins when compared to the traditional business.

1GW Solar/Wind power project in India through AMNS JV; started commissioning in 3Q 2024

554 MW Wind power project in Brazil through Casa dos Ventos JV; expected to commission in 2025

130MW Solar/Wind Power project through PCR JV. Commissioned in Dec 2023.

8. Debt profile and Capital requirements

AM paid close to 800M$ in interest payments in 2023. If interest rates decline, this will add to the bottom line. The debt pay-down schedule can be manageable, I don't see any bankruptcy risks.

Source: Annual Report - 2023

M&As and Divestments

The company is acquiring assets in the USA, and expanding in India and Brazil. Occasionally divests low-performing assets.

ArcelorMittal has agreed to buy a 28.4 percent equity interest in Vallourec, a France-based producer of recycled-content steel pipe and tube with electric arc furnace (EAF) melt shops in Brazil and in Ohio. ⇒ Though AM has the existing relationships with Vallourec, I am unable to understand the rationale for the minority investment. This acquisition will add 150m$ of EBITDA for AM’s share.

9. Risks

Let's look at what are the risks with investing in AM.

China exports/dumping low cost products for prolonged period

As the Chinese economy is going through a slow-down, the Chinese steel manufacturers are exporting the steel to other countries like India and Brazil. India, Brazil and Mexico started imposing anti-dumping duties to level the playing field to the local steel manufacturers.

The industry believes that Chinese manufacturers are currently losing money, and cannot sustain this over a long term.

Labor accidents and strikes

The Kazakhstan mine accident resulted in the death of 46 employees which also accelerated the sale to Kazakhstan's government. Most of the employees are represented by labor unions and can disrupt company operations.

Asset impairments in certain geographies

Got operations in 15 countries with different rules of law. As the steel manufacturing is done at high temperatures, there can be accidents which may result in large penalties and closure of certain facilities.

In Italy, the steel plant is currently not running as there is a court dispute on-going between AM and the Italian Govt. Though AM owns 62%, the Italian Govt. is planning to take over the control of the steel plant.

High Capex requirements for De-carbonization

Europe is pushing for Green steel manufacturing along with the other developed countries. This will result in high intense capex cycle for the next two decades.

10. Summary

Best-case scenario by 2030: 10x

12B$ of EBITDA on average by increasing the value added products mix.

8x multiple (multiple expansion from 5 to 8) will result in 12x8 = 96B$

Share buyback of approximately 50% will result in EPS multiple by 2. 96x2 = 192B$

Average-case Scenario by 2030: 6x

In the normalized environment the earnings are expected to be 20-25% higher. In the next 7 years, the decarbonization capex will generate higher EBITDA of 1.8B$ by 2026, and subsequently the company can generate 10B$ of EBITDA (6.5B in 2023 + 1.8B additional earning by 2026 + 1.7B$ from the capex from 2027 and inflation) in a bad environment in 2030. With 5x multiple 50B$ market cap would mean ~3x from the current market price and share count reduction by 50% through share buybacks would result in 6x return by 2030.

Worst-case Scenario by 2030: 2.5x

The company is struggling due to Chinese dumping of steel due to the Chinese economy slow-down, and only the EBITDA goes to 8B$. With 5x multiple, the market cap is 40B$.

The share count is only reduced by 25%, increasing EPS will give 50B$ valuation. Overall the investment will produce 2.5x return.

References:

2023 Annual Letter: https://corporate.arcelormittal.com/media/qwghoup1/annual-report-2023_combined.pdf

2022 Annual Letter: https://corporate.arcelormittal.com/media/s2xdue0a/annual-report-combined-2022.pdf

2021 Annual Letter: https://corporate.arcelormittal.com/media/xm4blr5z/annual-report-combined-2021.pdf

2024 Q1 Presentation: https://static.seekingalpha.com/uploads/sa_presentations/994/101994/original.pdf

Legal Disclaimer

The information provided on this blog is for educational and informational purposes only and should not be construed as financial, investment, or legal advice. NurtureWealth Capital, LLC and its affiliates do not provide personalized investment recommendations, and any opinions expressed herein are solely those of the author.

Investing in stocks involves risk, including the potential loss of principal. Readers should conduct their own research and consult with a licensed financial advisor before making any investment decisions. Past performance is not indicative of future results.

This blog may contain forward-looking statements based on current market conditions, expectations, and assumptions. These statements are subject to risks and uncertainties that could cause actual results to differ materially.

NurtureWealth Capital, LLC does not guarantee the accuracy, completeness, or timeliness of the information presented. The author and NurtureWealth Capital, LLC may or may not hold positions in the securities discussed.

By accessing this blog, you agree that NurtureWealth Capital, LLC shall not be held liable for any direct or indirect losses arising from the use of the information provided.

Always perform your own due diligence before making investment decisions.