Fluence Energy: A BESS (Battery Energy Storage Systems) play

“We're only as good as our next investment.” - Roelof Botha, Managing Partner and Steward of Sequoia Capital

Investment Summary: Fluence Energy (FLNC) provides Battery Energy Storage Systems (BESS) built using Lithium-ion batteries across the world. The company is trading at 3B$ market cap. At the time of writing the company has ~500M$in cash. The company raised 350M$ of convertible notes (debt) during Dec 2024, resulting in the effective Enterprise Value of 2.85B$.

The BESS industry has huge tailwinds as part of the energy transition megatrend expected to last for multiple decades, FLNC is expected to grow 50% revenues in 2025, and I expect the growth to continue at ~30%.

By the end of fiscal 2025, the ARR (Annual Recurring Revenue) is forecasted to be at 145M$ per annum consisting of digital (75%) and battery services (25%). In the next 10 years, the ARR revenues expected to grow to 1B$ assuming 25% CAGR as per my forecast which makes FLNC a great investment.

Business & History

Fluence Energy (NASDAQ:FLNC) was initially formed as a joint venture between Siemens Industry Inc, and AES Corporation in June 2017. The company went public through IPO in Nov 2021.

Fluence is a global market leader delivering intelligent energy storage and optimization software for renewable and storage. FLNC primarily operates in utility-scale battery storage solutions along with industrial opportunities. FLNC operates in 50 markets across the globe with 5.0 gigawatts of energy storage assets deployed as of Sept 30, 2024.

Three revenue segments

Energy Storage solutions - primarily consists of manufacturing and installation of battery storage systems including batteries. The battery products include Gridstack Pro, Gridstack, Sunstack, Edgestack, Ultrastack catering to different customer segments. Fluence Energy customers include power generation, utility, industrial and commercial customers.

Services - recurring O&M services that energy storage solutions require and asset management services that are provided by 3rd parties when asset owners outsource their operations.

Digital applications and Software - Cloud-based software to help asset owners to optimize the performance of their systems. The digital applications and software economic model is primarily structured as (i) $/kilowatt (“kW”) recurring fixed fees, and in some cases (ii) $/kW performance-based incentive fees both calculated based on the GWs of storage and generation assets on which digital applications and software service offerings are deployed.

Ownership: Currently AES Grid Stability owns 28.5% of economic interest in FLNC with 66.6% voting power whereas Siemens owns 28.5% of the economic interest and 13.3% of voting power.

Founded by AES (a global energy company) and Siemens in 2018, Fluence has projects in 30 markets around the world. Its global experience, modular products and sophisticated software enable its customers to modernize electric grids and accelerate local renewable deployment while maintaining reliability.

2. Why do we need BESS (Battery Energy Storage Systems)?

1. Balancing Supply and Demand

Peak Shaving: BESS helps manage peak electricity demand by storing energy during off-peak periods and releasing it during high-demand times, reducing strain on the grid.

Load Leveling: Smoothens fluctuations in energy demand, ensuring a consistent and reliable power supply.

2. Integrating Renewable Energy

Energy Storage for Intermittency: Solar and wind energy are intermittent (day/night cycles or variable wind speeds). BESS stores excess energy generated during peak production and releases it when production drops.

Grid Stability: Mitigates the variability of renewables by maintaining a consistent power output.

3. Enhancing Grid Stability and Resilience

Frequency Regulation: BESS responds rapidly to fluctuations in grid frequency, helping maintain grid stability.

Voltage Support: Provides reactive power to stabilize voltage levels in the grid.

Black Start Capability: Allows the grid to restart quickly after a blackout by supplying initial power without relying on other generators.

4. Deferring Infrastructure Investments

Reduced Need for Grid Upgrades: By managing peak loads and storing energy locally, BESS reduces the need for expensive transmission and distribution system upgrades.

Localized Energy Storage: Serves as a distributed energy resource (DER) that enhances local grid reliability without extensive infrastructure.

5. Supporting Decarbonization Goals

Reducing Fossil Fuel Dependence: Enables utilities to rely less on fossil fuel-based peaking plants, which are often expensive and emit high levels of CO₂.

Enabling 100% Renewable Goals: Facilitates the transition to clean energy by ensuring reliability and availability.

6. Economic Benefits

Energy Arbitrage: Utilities can store energy when prices are low and sell it during peak times when prices are higher.

Ancillary Services: BESS can participate in ancillary service markets, providing frequency regulation and other grid services, generating additional revenue.

7. Emergency Backup Power

Power Reliability: During outages, BESS provides backup power to critical infrastructure, ensuring essential services remain operational.

3. BESS demand outlook

Energy Demand Across the globe:

US electricity demand is projected to rise ~15-20% in the next decade, driven primarily by AI data center growth, domestic manufacturing. India’s energy demand is expected to grow by 35% by 2030. Europe’s energy consumption is expected to grow by 7% by 2030.

As the energy demand grows, the share of renewables is set to grow. The EU and USA are both forecast to double the pace of renewable capacity growth between 2024 and 2030 [1].

Renewables plus storage is displacing thermal generation and can be deployed significantly faster than other energy generation sources such as natural gas and nuclear.

BloombergNEF currently estimates in its 2H 2024 Energy Storage Market Outlook, published in November 2024, that the global utility scale market, excluding China, will add approximately 2,529 GWh between 2024 and 2035.

BloombergNEF New Energy Outlook 2024

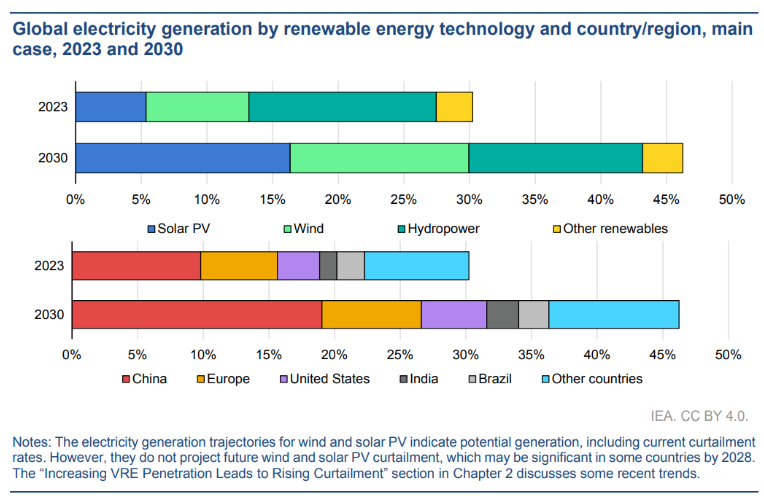

Solar and Wind renewable energy generation expected to increase significantly in the coming years whereas China continues to play the dominant role in renewable energy generation.

IEA forecast of global electricity generation

95% of the renewable electricity capacity additions are based on Solar and Wind, and it continues to stay in the range as the renewable energy capacity to reach 900 GW by 2030.

IEA forecast of Renewabale electricity capacity additions

High VRE (Variable Renewable Energy) consisting of Solar+Wind energy volumes have led to the potential need for energy storage to balance the system, provide ancillary services and reduce economic and technical curtailment. We estimate that over 540 GW of standalone battery storage projects are currently in grid connection queues in the United States, the United Kingdom, Australia, Spain and Chile. Of this capacity, over 55 GW is in late-stage development, with the United States having the highest amount (64%), followed by Spain (19%), the United Kingdom (12%), Australia (5%) and Chile (less than 1%). [IEA Report]

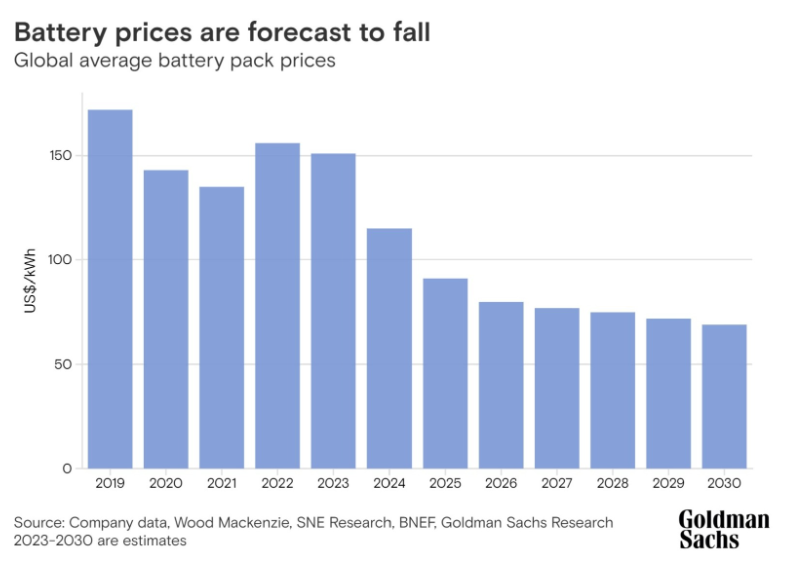

According to data from the U.S. Department of Energy, the cost of lithium-ion batteries for electric vehicles has decreased by approximately 90% over the last decade, with the most significant drop occurring between 2008 and 2023.

Key points about the cost decline:

Percentage drop: Around 90%.

Cost per kWh in 2008: Approximately $1,355.

Cost per kWh in 2022: Around $153

Goldman Sachs forecast of Battery prices

Overall, there is a strong demand for BESS in the coming decades driven by multiple factors which provide great tailwinds to Fluence Energy.

4. Business Parameters

| Business Parameter | Value | Comments |

|---|---|---|

| Market Cap | $ 2.9B | At share price $16.1, market cap is $2.9B |

| Enterprise Value | $ 2.7B | |

| Debt Cash Net Cash |

~390M (38M $ + 350M $ new debt issued) 520M $ ( liquidity) $130M |

The company requires higher working capital as the project intake grows. |

| Revenue Growth (1, 3, 5 Years) | 22%, 58% , 97% | Several utility projects got delayed in 2024 due to high interest environment. |

| Operating Income (EBIT) (1, 3, 5 Years) | 26.6M, -112M, -284 | |

| Cash from operations in 2024 | $ 80M | |

| Gross Margin | 12.9% FY24 | Forecast of 10-15% for FY25 |

| Capex Guidance/Working Capital forecast | 300-350M$ for working capital and manufacturing line at AESC |

5. Management

CEO is Julien Nebreda, CFO is Ahmed Pasha are long term employees at AES (Fluence Energy Parent Company). The other senior executives like Chief Strategy Officer and Chief Legal Officer are from AES as well. I am neutral about the management. The gross profits improvement in the recent quarter demonstrates that the company is focussing on profitable revenue growth.

News on FLNC:

Blue Orca Capital published a short report in which Siemens Energy, the U.S. affiliate of Fluence's largest shareholder and corporate parent, Siemens, had filed a lawsuit against it. The lawsuit accuses Fluence of "a laundry list of embarrassing and costly engineering and design failures as well as knowingly false representations and omissions." It further stated that the lawsuit explains why Fluence's largest shareholder, Siemens, has ceased to be a major customer and has begun to sell its shares.

Fluence energy called the short report as blatant misrepresentation and published the following clarifications (https://ir.fluenceenergy.com/news-releases/news-release-details/fluence-responds-misleading-short-seller-report):

The short-seller's report references pending litigation between Fluence and Siemens Energy, attempting to characterize it as a "critical and dramatic development." While any dispute with a customer is unfortunate, this is a small, ordinary course of commercial dispute arising from a single project. Fluence brought the action to collect approximately $2 million in unpaid amounts due, and Siemens Energy responded with counterclaims of approximately $9 million. Fluence strongly denies Siemens Energy’s counterclaims and the case is progressing in the ordinary course.

Siemens AG and its German retirement fund are investors in Fluence. Siemens AG has a minority ownership interest in Siemens Energy – it is not the same company and there is no legal case between Siemens AG and Fluence. We believe the litigation with Siemens Energy has no effect on our strong relationship with Siemens AG.

The short-seller's report wrongly implies AES is moving away from Fluence as a supplier. In fact, Fluence continues to be AES’ preferred Battery Energy Storage Systems technology provider. Our robust pipeline of sales to other customers continues to grow. Contrary to the implications in the short-seller report, the diversification of our customer base reflects the financial strength of our business and is part of our long-term strategy.

Fluence management showed consistent focus on profitability and Gross margin forecast is in the 10-15% range in the coming years. As the company acts as a system integrator, the margins are narrow. The company demonstrates to maintain the positive gross margins with disciplined order intake.

Q4 FY2024 Investor Presentation

6. Company Focus

AES started working on BESS since 2008, Fluence Energy established in January 2018 as a joint venture between Siemens and AES. Since then, it continued to evolve, grow, and expand business and operations, completing the IPO in the first quarter of fiscal year 2022

As of September 30, 2024, FLNC deployed energy storage products and solutions in 33 markets in 25 countries. FLNC sell our energy storage solutions, services, and digital applications to a wide range of customers around the world, including utilities and load-serving entities, IPPs, developers, conglomerates, and C&I customers. In fiscal year 2024, the two largest customers represented approximately 50% of our revenues. In addition, as of September 30, 2024, approximately 41% of our revenue was with related parties, primarily AES and its affiliates. As of September 30, 2024, the Company had $4.5 billion of remaining performance obligations related to our contractual commitments, which we refer to as our backlog, of which 16% is with AES.

As of September 30, 2024, FLNC had a gross global pipeline of 115.9 GWs, which includes 51.4 GWs for energy storage solutions and services. Of the energy storage solutions and services global pipeline, United States customers composed the largest portion of our pipeline at 14.5 GWs or approximately 28%, with Australia customers following at 8.6 GWs or 17%, and Germany customers at 7.2 GWs or 14%

Fluence Energy’s R&D, manufacturing Capabilities:

Gridstack Pro is designed to leverage our Fluence-designed Battery Packs for optimized system performance and supply chain agility. The Fluencedesigned Battery Packs combine state-of-the-art battery modules, management systems, and monitoring equipment into a unified product architecture designed to improve operations through advanced thermal and state of charge (SOC) management, which is intended to promote consistent product performance and safety at the system level. The Fluence-designed Battery Pack is intended to give Fluence greater control over our global supply chain and increase standardization across products. FLNC initiated domestic production of battery modules at its contract manufacturer’s facility in Utah in September 2024. These battery modules will incorporate battery cells manufactured in Tennessee for our domestic content offering.

Fluence Manufacturing Strategy:

The company strives to limit capital-intensive and low value-added activities. Fluence partners with the other contract manufacturers for battery pack components and manufactures systems in its own facilities. Fluence also innovates the products and solutions to minimize the amount of assembly by customers. I believe it's a preferred strategy to minimize the capital intensity required, and keep moving to the next upcoming battery technology if required.

7. Battery technologies and possible disruptions

Fluence Storage solutions are primarily built on Lithium ion batteries (LMP - Lithium Ion phosphate ) while the management is exploring the other upcoming technologies like

solid-state lithium

lithium manganese iron phosphate (LMFP)

lithium nickel manganese oxide (LMNO)

nickel hydrogen, all-iron flow, and iron-air batteries

The key risk in investing in Fluence Energy, its ability to adapt to the upcoming battery technology changes. Here’s a detailed comparison table highlighting key differences among various battery storage technologies:

Battery Storage Technologies Comparison

| Battery Type | Approx. Cost | Charging Efficiency | Discharge Efficiency | Energy Density (Wh/kg) | Life Cycles | Applications |

|---|---|---|---|---|---|---|

| Lithium Iron Phosphate (LFP) | $100–150/kWh | ~95% | ~95% | 90–160 | 3,000–10,000 | EVs, Grid Storage, Consumer Electronics |

| Solid-State Lithium | $200–400/kWh | ~98% | ~98% | 250–500 | 5,000–15,000 | Next-gen EVs, Aerospace, Portable Electronics |

| Lithium Manganese Iron Phosphate (LMFP) | $110–160/kWh | ~95% | ~95% | 150–190 | 3,000–6,000 | EVs, Grid Storage |

| Lithium Nickel Manganese Oxide (LMNO) | $150–250/kWh | ~90% | ~90% | 150–200 | 2,000–5,000 | High-Performance Applications, EVs |

| Nickel Hydrogen | $1,000–2,000/kWh | ~85% | ~80% | ~55 | 20,000+ | Aerospace, Satellite Systems |

| All-Iron Flow | $150–300/kWh | ~70–85% | ~70–85% | ~20–40 | 10,000+ | Long-Duration Grid Storage |

| Iron-Air | $20–30/kWh (projected) | ~50–70% | ~50–70% | ~100 | 500+ | Low-Cost, Long-Duration Grid Applications |

Lithium Iron Phosphate (LFP):

Advantages: High safety, long cycle life, stable thermal characteristics, relatively low cost.

Disadvantages: Lower energy density compared to other lithium-ion chemistries.

Solid-State Lithium:

Advantages: High energy density, long life cycles, improved safety (non-flammable).

Disadvantages: High production costs, still under development for large-scale deployment.

Lithium Manganese Iron Phosphate (LMFP):

Advantages: Higher energy density than standard LFP, better thermal stability, and lower cost compared to nickel-based chemistries.

Disadvantages: Less mature compared to LFP.

Lithium Nickel Manganese Oxide (LMNO):

Advantages: High power density and fast charging capabilities.

Disadvantages: Higher cost, lower cycle life, and thermal stability concerns.

Nickel-Hydrogen:

Advantages: Extremely long cycle life, reliable in harsh environments.

Disadvantages: High cost, bulky, low energy density.

All-Iron Flow:

Advantages: Long life cycles, low-cost materials, scalable for large energy storage.

Disadvantages: Low energy density, low efficiency.

Iron-Air:

Advantages: Ultra-low cost, suitable for long-duration storage.

Disadvantages: Low efficiency, still under research and commercialization.

Though there is an increased research in the Battery Energy Storage technologies, lithium-iron-phosphate batteries will play a dominant role in the upcoming decade as per the IEA forecast. FLNC primarily supplies LFP batteries as part of its BESS products.

IEA forecast on LFP battery usage

Apart from the above mentioned battery technologies, there are other energy storage technologies that are currently under development. Investor need to track how the other energy storage technologies which are evolving and assess the disruption risks to FLNC products.

Upcoming Energy Storage Technologies Comparison

| Technology | Efficiency (%) | Energy Density (kWh/m³) | Storage Duration | Applications | Key Advantages | Key Challenges |

|---|---|---|---|---|---|---|

| Compressed Air Energy Storage (CAES) | 40–60 | ~3–6 | Long-term (hours to days) | Large-scale grid storage | High scalability and durability | Requires specific geological formations |

| Thermal Energy Storage (TES) | 70–90 | ~50–200 | Medium to long-term | Renewable energy, district heating/cooling | Low cost, integration with solar plants | Thermal losses, material constraints |

| Liquid Air Energy Storage (LAES) | 50–60 | ~50–100 | Long-term (days to weeks) | Utility-scale storage | Environmentally friendly | Low efficiency, high initial cost |

| Gravity-Based Energy Storage (GBES) | 75–90 | ~2–5 | Medium-term (hours) | Renewable grids | Minimal degradation, eco-friendly | Large space requirements |

| Hydrogen Energy Storage (HES) | 30–50 | ~120–140 | Very long-term (weeks to months) | Energy storage and fuel | High energy density, versatile use | Low efficiency, expensive infrastructure |

| Thermo-Chemical Energy Storage (TCES) | 80+ | ~150–300 | Long-term | Industrial processes, renewable storage | High efficiency, industrial compatibility | High R&D costs, chemical safety |

8. Risks

Change in battery storage technology: The battery technologies are still evolving. Though LFP batteries are used dominantly today, it might change in future. The company should keep updating its technologies to the evolving technology environment.

Inability to scale to the customer demands: FLNC currently acts as a system integrator. The company only contracts key components like battery modules for the US, and procures the components from the other vendors. The company should maintain a balanced supply chain in order to timely deliver the projects for the utility customers.

Not adapting to the customer needs: Currently FLNC produces the battery storage modules that require no assembly at the site, and deploy the battery storage module as is. The company should produce the cutting edge products to compete with the companies like Tesla, Canada Solar etc.

Customer Concentration risk: In FY2024, the top two customers contributed 50% of the revenue. Customers moving away could impact revenues considerably.

10. Return Expectations

| Scenario | Probability | Expected Growth Rates | Returns in the next 10 years |

|---|---|---|---|

| Best | 35% | 50% year 1, 25% years 2-7, 20% Years 8-10 Digital + Services to grow 30% |

13x (30B + 10B) |

| Average | 45% | 25% for the years 1-5 and 20% for the years 6-10 | 9x (22B$ + 5B$) |

| Worst | 30% | 20% for the years 1-5, FLNC fails to adopt the new battery technology | 3x |

References:

IEA (International Energy Agency) report on renewables 2024:

https://iea.blob.core.windows.net/assets/17033b62-07a5-4144-8dd0-651cdb6caa24/Renewables2024.pdf

Guidelines to implement battery energy storage systems under public-private partnership structures, published by World Bank in January 2023. https://documents1.worldbank.org/curated/en/099536501202316060/pdf/IDU0edcfc32c0825f040f509c0b0bbf49294e569.pdf

Investor presentation Q4, FY 2024 https://ir.fluenceenergy.com/static-files/58ed5fe2-7d77-46c6-bb3e-a2fe09cd9b36

Form 10-K, FY 2024 https://ir.fluenceenergy.com/static-files/2ce83e3b-4a94-40f6-8c92-8540b657df80

Legal Disclaimer

The information provided on this blog is for educational and informational purposes only and should not be construed as financial, investment, or legal advice. NurtureWealth Capital, LLC and its affiliates do not provide personalized investment recommendations, and any opinions expressed herein are solely those of the author.

Investing in stocks involves risk, including the potential loss of principal. Readers should conduct their own research and consult with a licensed financial advisor before making any investment decisions. Past performance is not indicative of future results.

This blog may contain forward-looking statements based on current market conditions, expectations, and assumptions. These statements are subject to risks and uncertainties that could cause actual results to differ materially.

NurtureWealth Capital, LLC does not guarantee the accuracy, completeness, or timeliness of the information presented. The author and NurtureWealth Capital, LLC may or may not hold positions in the securities discussed.

By accessing this blog, you agree that NurtureWealth Capital, LLC shall not be held liable for any direct or indirect losses arising from the use of the information provided.

Always perform your own due diligence before making investment decisions.