Lumen Technologies: A turn-around story

“The only rule I have is there are no rules.” - Rakesh Jhunjhunwala

Business & History

Lumen Technologies(NYSE:LUMN) is a traditional telecom company, formerly known as CenturyLink. Lumen's primary business is to provide Broadband (Fiber and Copper) services and it also has legacy Voice, VPN services which are fast declining.

LUMN grew by acquiring several other companies, and during the process it acquired a significant amount of debt (37B$ debt by Dec 2017). As of Q1 2024, LUMN has debt of 19.5B$ and market cap of 1.3 B$ (as on 5/24/2024). I know that many investors will drop this company by just looking at this debt and market cap numbers. Stick with me if you can as I take you through the LUMN’s turn-around story.

Current Businesses: LUMN primarily offers Broadband services in two segments

Core Broadband services using National & International Network ⇒ Caters to Hyper-scalors, Govt. agencies, Enterprises etc.

Mass Markets ⇒ Caters to Retail customer with last-mile connectivity

There are several demand driving factors for connectivity, and some of them include

Hyper-scalar compute including AI/ML, AR/VR

Cloud based Apps and Services

Decentralized Architecture like Hybrid Cloud and Edge Solutions

Low-latency network for 5G and Autonomous driving

Growing demands to improve Customer Experience (Video, Voice, E-commerce, Data Transfer) etc.

LUMN has wide coverage of the Fiber network with a replacement cost of 150B$. Once a conduit is deployed in the ground, adding another cable is a relatively simpler task than installing a new conduit altogether.

Source: Lumen Q1-2024 Financial Results Presentation

The following picture demonstrates Lumen’s global network, and the orange dots indicate Lumen’s and Partner Colocation Data Centers.

Verizon’s Global Network.

2. Business Parameters

Market Cap : $ 1.2B

Enterprise Value : $ 18.5B

Debt - $ 19B, Cash available : $ 1.5B

Revenue Growth (1, 3, 5 Years) : -15%, -12 %, -9 % (Revenues were declining)

Operating Income (EBIT) Growth (1, 3, 5 Years) : -72% , -42% , -29 %

Cash from operations in the last year : $ 2.7B

Gross Margin (TTM, 5Y AVG) : 50.5%, 55%

EBIT Margin(TTM , 5Y AVG) : 5.29%, 17.5%

Capex Guidance : $2.7 - 2.9B (Capex spending to continue till 2027)

3. New Management

Telecom business is a low-growth matured industry, and all its peers in the industry are returning cash to the shareholders through dividends. LUMN board hired Kate Johnson in Nov 2022 who worked in the technology industry, and joined LUMN from Microsoft. Kate came with a two-step turn-around plan

Invest and grow the optical Broadband business

Build a brand new digital services business on top of the Broaband network.

Source: Lumen Q1-2024 Financial Results Presentation

Kate hired senior executives like Satish (AWS), Dave (PacketFabric and Cisco) to build the digital services business from scratch.

Source: Lumen Q1-2024 Financial Results Presentation

LUMN acquired several companies over the years, and was running diverse IT systems as is. Kate launched the consolidation of IT systems across LUMN to ONE system which helped in improving employee productivity and reducing operating costs.

4. Focusing on Growth segments

LUMN classified their existing business into three segments

1. GROW- High CLV (Customer Lifetime Value), to grow in future

2. NURTURE - No growth, moderately declining business

3. HARVEST - Fast declining business

Source: Lumen Q1-2024 Financial Results Presentation

Lumen is tilting the business towards GROW by investing in Capex and actively transitioning the existing HARVEST customers to Grow Services.

Currently the revenue decline in Harvest and Nurture businesses is higher than the growth in GROW business. The management expects the revenue declines should stop from H2 2024 and gradually grow from 2025 onwards.

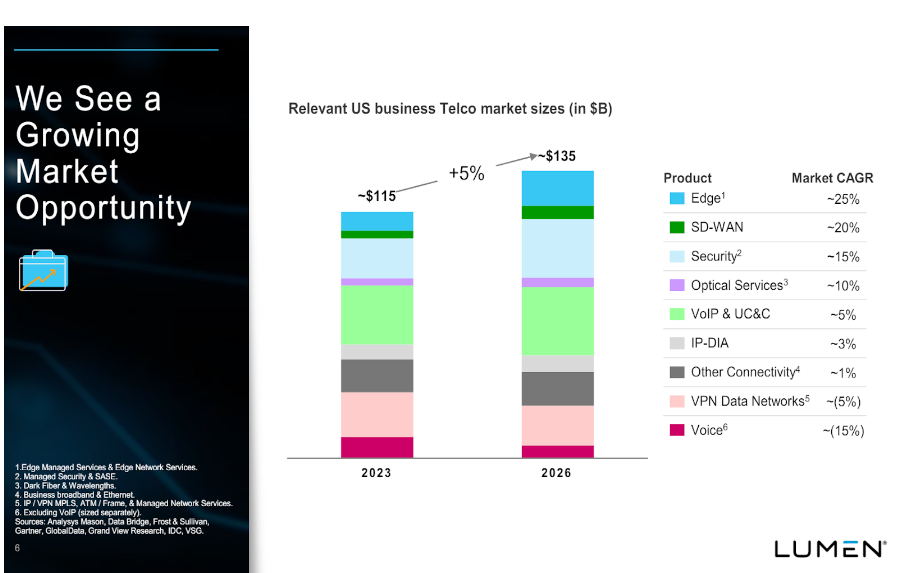

5. Digitalization Story

Source: Lumen 2023 Investor Day Presentation

The traditional optical Services tend to grow 10% CAGR in the next 3 years whereas the value-add services like Edge Managed Services, SD-WAN, Security tend to grow at higher growth rates at 25%, 20%, 15% respectively. LUMN is positioning itself to participate in the Value-added digital segment services. Historically the participants of this industry are technology companies, but not the traditional telcos. In the case of LUMN, its building vertically integrated value-add services.

NaaS (Network as a Service) would allow customers to scale-up and scale-down the network bandwidth as required rather than signing a long term contract which is not used most of the time. This will also help LUMN to monetize the existing broadband network.

Edge Deployments for low-latency solutions. The customers can rent the edge computing resources for deploying their solutions.

Turn-key cloud based collaboration solutions for Teams, Zoom and Webex

LUMN is partnering with SD-WAN service providers like Cisco, Fortinet, VMWare, HPE, Versa etc. to provide comprehensive SD-WAN solutions. The SD-WAN solutions leverage Lumen’s digital infrastructure including its security solution Lumen Defender.

Cybersecurity solutions

The following picture demonstrates the features of LUMN business segments when compared to today.

Future projection of Lumen’s market segments

Lumen is building vertically integrated digital solutions like NaaS, SD-WAN, API driven network customization etc.

6 Innovation & Security Solutions

Source: Lumen Q1-2024 Financial Results Presentation

ExaSwitch: Lumen’s ExaSwitch allows bandwidth scale-up and scale-down when hyperscalers connect data centers. Lumen deployed the ExaSwitch product to the large cloud customers like Google, Microsoft and another large cloud customer. This is a differentiated solution for the cloud customers to scale-up and scale-down bandwidth to cater to the demanding work-loads spread across data centers.

Source: Lumen Web-site

Lumen NaaS (Network as a Service):

Lumen offers integrated NaaS solutions where the solution is usually developed by Technology companies instead of start-ups. The NaaS will help LUMN to better monetize the underlying broadband network. By 2027, NaaS market SAM is expected to be 25-35B$.

Source: Lumen Q1-2024 Financial Results Presentation

Kate Johnson during JP Morgan Technology Conference “Lumen Digital is basically our R&D arm that is building new digital capabilities to transform the customer experience in networking. But I look at it as there are at least three places where telco ceded innovation to digital upstarts. They ceded it to tech, and it's in connectivity, security and communications or voice. And we have a right to win there because of our assets, because of our intellectual property. And with this play to win mindset and with this belief system that the customer experience is the product, we’re now going after those markets. And just a couple of examples. Like this whole NaaS and ExaSwitch, are virtual private fabric for customers to consume network services. Who else is doing that? Megaport and PacketFabric are two examples of companies that have high valuations that are completely digital, but they don't even own the network. They provide network-as-a-service and they lease their fiber from us.”

Lumen’s Cyber Security Solution:

Lumen’s in-house Black Lotus Labs developed SASE solution to defend against Cyber security attacks. Secure Access Service Edge (SASE) is a cloud-based security architecture that combines network connectivity and security functions into a single cloud platform. As Lumen owns the large network footprint, it is leveraging the network to detect DDoS (Distributed Denial of Service) attacks, and stop such attacks. DDoS is a powerful attack launched by distributed bots to bring down a network.

Lumen Defender is a patented product that proactively blocks evolving threats at the network edge before they can compromise a business’s network perimeter. Black Lotus Labs, Lumen’s threat research team, leverages its unique visibility into Lumen’s global internet backbone using ML algorithms to generate threat intelligence that detects malicious infrastructure being used by cybercriminals and nation state actors. [Lumen Website]

Lumen successfully identified and defended DDoS malware attack TheMoon. Now Lumen started monetizing the security solution, and started selling it as a value-added solution.

Kate Johnson during JP Morgan Technology Conference “We took Black Lotus Labs, their data algorithms and various machine learning models. And we said, hey, we are really good at identifying bad actors on the Internet. And we've done that 8 times for the United States government over the past couple of months. Why don't we package up that capability in the form of a service, a digital service to make it available to all enterprises. This is the kind of innovation that we did every day in tech that is net new for telco. And so we have a right to win in those spaces, and we are doing it and making a huge amount of progress. It's super exciting. And all of that is that new profit pools for us.”

Lumen partnered with SD-WAN solution providers like Versa to offer comprehensive security solutions at multiple layers to enterprise customers.

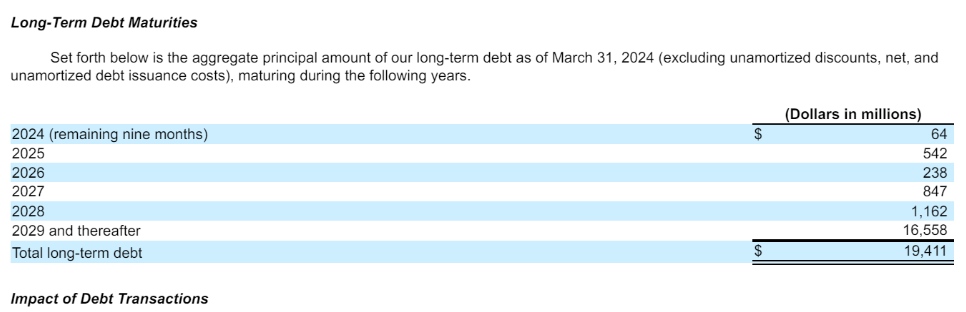

7. Debt profile and Capital requirements

There is no question that LUMN comes with a boat load of debt of 19.5B$, and hence the company is trading so cheap. The management mentioned that they were not winning the deals from their key customers as the customers see the large debt maturity in 2027 is a key risk to LUMN.

LUMN worked with its lenders and came to an agreement to push out the debut maturities.

Source: Lumen Q1-2024 Financial Results Presentation

Source: Lumen Q1 2024 10-Q

Debt restructuring pushed off repayments to 2029 and beyond, but this comes with an additional cost of 200M$ per year to the operational costs.

Reducing Debt: Lumen sold EMEA and Latin American assets over the past 2 years and brought down the debt from 29B$ in Dec 31 Debt to 19.5B$ debt as on 31st March 2024.

The debt will stay around the same for the next 1 or 2 years as the company is aggressively investing in the growth segments of the business. The management committed to sell/de-merge the “Mass Markets” business when the economic environment gets better.

The capex intensity in the range of 3-3.5b$ to continue until 2027.

Source: Lumen 2023 Investor Day Presentation

8. Past and Future Divestments - Mass Markets

Lumen divested several non-core assets in EMEA and Latin America to reduce its debt burden. Lumen management highlighted that they will be divesting ‘Mass Markets’ segment where the investment payoff period is very long (close to 10 years) and its commoditized segment. Lumen to focus on Business services and solutions where the capex pay-off period is close to 3 years.

Source: Lumen Q1-2024 Financial Results Presentation

In the Mass Markets business there are three segments. The Fiber Broadband business is growing while the other legacy copper and voice businesses are declining. The Fiber Broadband business generated 170M$ in Q1 2024, and growing, I expect the Fiber Broadband business to generate 800M$ of annualized revenue and should result in at least 8-10B$ if sold in a good environment. This sale should help in eliminating approximately half of the debt.

9. Risks with investment in LUMN

Let's look at what are the risks with investing in Lumen.

High Debt - 19.5B$

The company has to pay 1.3B$ of interest every year, and require it to generate sufficient cash flow to reduce the debt. The revenue growth should be higher to offset the declines in legacy business (copper broadband and voice).

Source: Lumen Q1-2024 Financial Results Presentation

Unable to divest Mass Markets division to reduce debt

In the next 3-4 years(by 2027), Lumen should divest the business to bring down the debt burden by a substantial amount.

Capex spending going beyond 2027

Lumen is currently investing in the Capex for both the Core business and Mass Markets business, and expects to significantly reduce the Capex spend from 2027 onwards. In the past years Lumen didn’t spend sufficiently in Capex as a large portion of the cash flow went in paying dividends. Slowing down the Capex from 2027 will also help in reducing the debt burden.

Source: Lumen 2023 Investor Day Presentation

Digital Services Execution

Lumen management is currently not guiding any revenue from the new Digital Services business. Increased R&D spend in the Digital Services business must result in additional revenues so the debt burden can be reduced.

Management Change Risk

If the company management changes and the direction is changed then the turn-around of LUMN might not happen.

10. Summary

Best-case scenario in 2033 (10 years from now):

Lumen is able to divest Mass Markets business at the valuation of 8B$, continued to execute on core optical network solutions, and moderate success with digital services.

5B$ in operating earnings (4B$ from the core services and 1B$ from digital value-add services like NaaS, Security Solutions etc.) and 10B$ of debt.

EV(Enterprise Value) = 10x multiple of OE = 5*10 = 50B$

Subtracting 10B$ debt from EV= 50-10 = 40B$ Market cap in 2030.

With the current market cap of 1.3B$, the company may give a 30x return.

Average-case Scenario in 2033 (10 years from now):

Lumen is unable to sell Mass Markets business. No meaningful success with Digital Services business and just continued with the core business and Mass Markets.

Operating Earnings in 2030: 3B$ (2.5B$ from core and 0.5B$ from Mass Markets)

Debt only reduced marginally to 15B$

EV = 8x multiple of OE = 8 * 3 = 24B$

Subtracting 15B$ debt from EV= 24-15 = 9B$

With the current market cap of 1.3B$, the company may give a 7x return.

Worst-case Scenario

The Worst-case scenario is management screwing up the basic execution and driving down the revenues. Due to high debt, the equity portion is erased and your investment will become zero.

The probability of this scenario is low, and Lumen has the hard assets

References:

Lumen Investor day 2023 presentation: https://s24.q4cdn.com/287068338/files/doc_presentations/2023/08/Lumen-2023-Investor-Day-Presentation.pdf

Lumen Q1 2024 Presentation: https://s24.q4cdn.com/287068338/files/doc_financials/2024/q1/Lumen-1Q24-Earnings-Presentation.pdf

Legal Disclaimer

The information provided on this blog is for educational and informational purposes only and should not be construed as financial, investment, or legal advice. NurtureWealth Capital, LLC and its affiliates do not provide personalized investment recommendations, and any opinions expressed herein are solely those of the author.

Investing in stocks involves risk, including the potential loss of principal. Readers should conduct their own research and consult with a licensed financial advisor before making any investment decisions. Past performance is not indicative of future results.

This blog may contain forward-looking statements based on current market conditions, expectations, and assumptions. These statements are subject to risks and uncertainties that could cause actual results to differ materially.

NurtureWealth Capital, LLC does not guarantee the accuracy, completeness, or timeliness of the information presented. The author and NurtureWealth Capital, LLC may or may not hold positions in the securities discussed.

By accessing this blog, you agree that NurtureWealth Capital, LLC shall not be held liable for any direct or indirect losses arising from the use of the information provided.

Always perform your own due diligence before making investment decisions.